The Statutory Residence Test (SRT): What It Means for Your UK Tax Position

If you live and work in the UK, you are almost certainly ‘resident’ there for tax purposes and probably have to pay tax in the UK on your world-wide income and gains. However, if you live or work abroad, you have the possibility of benefitting from ‘Non-Resident status’. Your residence position is the single most important factor which determines the reach of the UK tax system into your incomes, gains and assets. It is the fundamental building block on which international tax planning is built.

Consequently, it is vital to get your position right and, thus, to have a good grasp of the rules as they impact you year on year. Getting it wrong can have seriously adverse consequences. Getting it right can have a life-changing and long-term positive impact upon your finances.

The Statutory Residence Test (SRT) is the legal framework that gives you a clear, objective answer on whether you are UK tax resident or not in any given tax year.

This guide walks you through how it works, the day-counting rules and principles which can catch many people out, and the points where specialist advice pays for itself.

What is the Statutory Residence Test?

The Statutory Residence Test (SRT) is the legal framework that determines whether you are resident in the UK or not for a given tax year. Enacted into law by Schedule 45 of Finance Act 2013, it took effect from 6th April 2013, replacing an archaic case-law based system of common law rules that had produced consistently uncertain outcomes for over 200 years.

The SRT applies independently for each UK tax year (6 April to 5 April). An individual can be UK resident one year and non-resident the next. UK tax residents are generally taxed on their worldwide income and gains (unless FIG/OWR or Double Tax Treaty relief applies); whereas, non-residents typically pay UK tax only on UK-source income and certain UK gains. If you have been Non-Resident for long enough, your non-UK assets can also fall outside of the reach of Inheritance Tax. Non-Residents can also enjoy relief from UK tax on certain UK incomes where a Double Tax Treaty exists with the country they are living in. The distinction can be worth a great deal for individuals with international employment, investments, or assets.

Why Does the SRT Exist?

Fundamentally, the ‘old system’ was very broken and the then Government wisely decided that individuals and businesses needed rules-based certainty, so they could plan with confidence. The law as it previously stood comprised of only three short paragraphs and was becoming increasingly unfit for purpose, especially in the modern world where people cross borders so easily. Over the centuries a large body of case law had developed, some of which was contradictory and confusing, often resting on fine judgments about semantics. The Inland Revenue (as it was then called) produced ‘guidance’ and rules upon which people relied but which, because they were simply informal opinions, turned out to be consistently untrustworthy.

The case of Robert Gaines-Cooper is a case in point. Gaines-Cooper was a British businessman who had spent fewer than 91 days per year in the UK from 1976 to 2004 and had his home in the Seychelles. Based on HMRC’s published guidance at the time, he believed this day count made him non-resident. It did not – the court and subsequently the Court of Appeal found that, alongside his clear residence in the Seychelles, he also ‘resided’ in the UK – a ruling that eventually left him liable for millions in back taxes.

The system needed to change, to be made clear and to produce outcomes which are legally-binding on both the individual and HM Revenue & Customs. One might make the argument that the SRT is needlessly complex – indeed HMRCs original guidance notes ran to over 100 pages – and there are still some areas of uncertainty where careful interpretation is needed. However, SRT is a huge advance on the previous system. It is broad enough to apply clearly to every situation, is generous enough in its provisions to allow for clear and unmistakable routes to Non-Resident status and, at the same time, has been drafted to be faithful to the core principles established by the previous body of case law.

Here at Spice Taxation, we are huge fans of the Statutory Residence Test, for the clear outcomes it produces. Care is still very much needed though and the purpose of this guide it to help you to clarity.

The Impact of SRT on Expats

For British expats, the SRT determines whether HMRC can tax your overseas salary, foreign rental income, gains on investments held abroad, and ultimately your estate, or whether those assets are entirely outside the UK tax net.

The impact is sharpest during transitions: the year you first leave the UK, the year you return, or any year when circumstances shift or in years when you unexpectedly have to spend more time in the UK. A promotion that keeps you in the UK for additional weeks, a spouse who returns ahead of you, or a property held for family visits can all be enough to impact the outcome

For expats in Singapore, Dubai, Hong Kong, or other international hubs, the SRT also interacts with local tax regimes. Singapore taxes income on a territorial basis: British expats resident there typically pay no Singapore income tax on offshore income. Remaining UK resident, or becoming UK resident again, brings that same income into the UK tax charge.

For most British expats, non-UK residence is the preferable outcome. Achieving and maintaining that status depends on applying the SRT correctly each year.

Am I a UK resident?

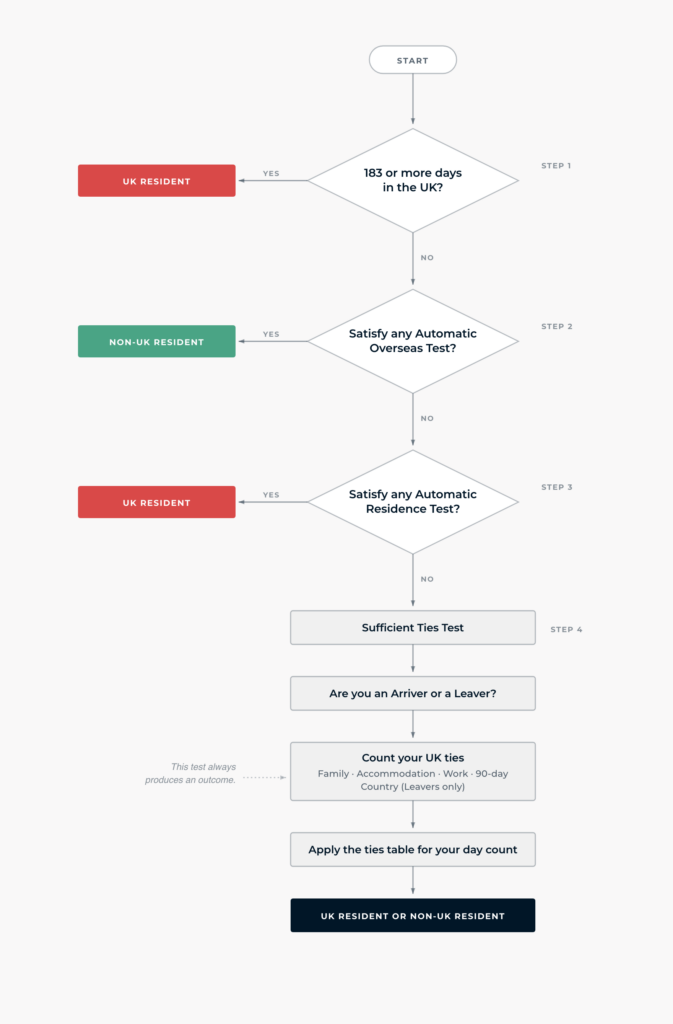

The simplest case: spend 183 or more days in the UK in a tax year and you are automatically UK resident, regardless of everything else. This is known as the First Automatic Residence Test.

If you spend fewer than 183 days in the UK, the answer depends on prior residence history, work patterns, home arrangements, and ties to the UK. There are three broad ways the question gets resolved: the Automatic Residence Tests (which make you UK resident regardless of day count), the Automatic Overseas Tests (which make you non-resident regardless of other factors), and the Sufficient Ties Test (which weighs your day count against the number of connections you maintain with the UK).

The tests apply sequentially starting with the Automatic Overseas Test, then moving to the Automatic Residence Test and then, if no outcome has been achieved, the Sufficient Ties Test as the tie-breaker. Where you get a conclusion at a part test, you stop – that is your outcome for that tax year, regardless of any other factor.

UK Days (Days Spent in the UK)

The law talks about “days” spent in the UK. This is misleading. Throughout the Statutory Residence Test a day qualifies as “day” in the UK if you were physically present in the UK (territory, airspace or waters) at midnight Greenwich Mean Time. The date on which you depart the UK does not normally count as a day of presence, though there are some limited circumstances when it can.

For simplicity, we will refer to “days” in this article – but remember that the count is actually of midnights of physical presence in the UK.

There are two situations where a day in the UK does not count towards day-counting totals:

- Transit days: A day is not a UK day if you arrive as a passenger and depart the following day without engaging in activities unrelated to travel: no business meetings, no family visits, nothing substantial beyond the transit itself. For example, you land in Gatwick one evening and don’t leave until the following morning.

- Exceptional circumstances: Up to 60 days per tax year may be disregarded where the individual’s presence in the UK arose from circumstances genuinely beyond their control. Recent case law implies that being detained in the UK to discharge a moral obligation can also potentially qualify as exceptional.

The deeming rule: For individuals who were UK resident in at least one of the preceding three tax years and hold three or more UK ties, departure days (present in the UK during the day, but not at midnight, because the individual returns overseas that evening) count as UK days, but only after the first 30 such days in the tax year. This is to prevent a situation where someone is actually still living in the UK being non-resident but who makes very frequent trips into the UK for short periods.

So, with these basic principles established, if you have spent fewer than 183 days in the UK in a tax year, our starting point is to determine whether you qualify as Non-Resident under the ‘Automatic Overseas Tests’.

The Automatic Overseas Tests (AOT)

If you let out a UK residential (or commercial) property, the net rental profit is subject to UK Income Tax. This applies whether you are UK-resident or not. Rental profit must be declared through Self Assessment and you may have to make quarterly submissions to HM Revenue & Customs under the Making Tax Digital (MTD) rules.

Individuals

Rental profit is taxed at your marginal income tax rate: 20% at basic rate, 40% at higher rate, and 45% at additional rate. Rental income is added to your other income and taxed accordingly. Even modest rental income can be taxed at 40% or 45% if other income already puts you near the higher-rate threshold.

From April 2027, the Income Tax rates on property rental profits will rise by 2% to 22% at basic rate, 42% at higher rate, and 47% at additional rate.

At £1,000 rental income allowance can apply under certain limited circumstances.

We strongly recommend that all Non-Residents file an annual Tax Return or Form R43 to declare their rental income. It should be a Tax Return if you have taxable rental profit or if you have been sent a Tax Return or a Notice to File by HM Revenue & Customs. It should be the Form R43 if your rental profit, together with other reportable incomes, is within the level of your Personal Allowance.

British expats are entitled to a Personal Allowance. This is also the case for abroad category of other individuals, however the rules are complex and if you are not British, it is best to seek professional advice.

Please note that the Personal Allowance is only given if you claim it each year. This is one of the important reasons which you must file either a Tax Return or a Form R43 to report your incomes.

Trustees

Trustees pay Income Tax at the trust rate of 45% on rental profit, with up to £1,000 taxed at 20%. No personal allowance is available.

Companies

Companies pay Corporation Tax on rental profits: 25% for profits above £250,000, 19% for profits below £50,000, with marginal relief between the two. Unlike individual landlords, companies can still deduct mortgage interest in full as a business expense.

Allowable Deductions for Landlords

Individual landlords can deduct allowable expenses before calculating taxable profit:

- Mortgage interest costs: Not deductible directly from rental profit for individual landlords. A 20% tax credit applies on qualifying finance costs under Section 24. Higher-rate and additional-rate taxpayers receive less relief than the full cost of their mortgage interest.

- Maintenance costs: Repairs to keep the property in existing condition are deductible. Improvements that add value are not.

- Lettings agent fees and the VAT they charge: Fees for finding tenants, collecting rent, or managing the property are fully deductible.

- Insurance premiums: Landlord, buildings, and contents insurance paid by the landlord are deductible.

- Council tax where applicable: Council tax paid by the landlord during void periods is deductible.

- Utility bills where applicable: Gas, electricity, or water paid by the landlord during voids or where included in the rent are deductible.

Capital expenditure cannot be deducted from rental income, but may reduce your Capital Gains Tax liability on eventual sale.

The Automatic Residence Tests (ART)

Where no Automatic Overseas Test applies, the Automatic Residence Tests are considered. Satisfying any one means UK residence for the tax year, regardless of UK day count.

Second Automatic UK Test

Condition: All of the following must apply:

- A UK ‘home’ is available for 91 or more consecutive days, with at least 30 of those days falling within the tax year.

- You spend some time in that UK home on at least 30 days during the tax year.

- During the 91-day period, you either have no overseas home, or you spend fewer than 30 days in each overseas home.

It is important to note that the test here is not whether you were physically present in the property at midnight – the test is whether you spent any time at all in the property during the day, regardless of how short.

The term “home” is a really important one for the Statutory Residence Test and we will consider it further on.

In short, this test catches those who maintain a substantive UK base in the absence of a foreign equivalent and use it regularly, even where their total UK day count is low. Where an individual holds multiple UK homes, the test is applied to each in turn and is satisfied if the conditions are met for any single property.

Third Automatic UK Test

Condition: All of the following must apply:

- You work for sufficient hours in the UK, averaging 35 or more hours per week, across a 365-day period falling wholly or partly within the tax year.

- No significant breaks from UK work during that 365-day period.

- More than 75% of working days in the 365-day period are UK working days.

- At least one qualifying UK working day within both the 365-day period and the tax year.

The 365-day period can straddle two tax years, so this test can apply even where full-time UK work only began partway through the year under review. The 75% threshold means it is not enough that most working days are in the UK; the proportion must exceed three-quarters.

If neither the second nor the third automatic UK tests apply to you, we must move onto the Sufficient Ties Test which will always generate an outcome.

Sufficient Ties Test

First, we must identify whether you are an “Arriver” or a “Leaver”. Then we must determine which “Ties” apply to you for the tax year. The possible ties are: Family, Accommodation, Work, 90-day, and Country (the Country tie applies to Leavers only). When this known, the question of whether you are Resident or Non-Resident is answered by establishing whether your count of days spent in the UK during the tax year is below (Non-Resident) or above (Resident) the prescribed allowance. We will drill into this a little further down.

How the SRT Works in 4 Easy Steps (Flowchart)

As you can see, the SRT follows a logical decision sequence. Each step builds on the last, and the analysis ends as soon as a definitive answer is reached.

Defining Terms Used in the Statutory Residence Test

The SRT uses precisely defined terms. Applying them loosely is one of the most frequent sources of error. Each definition below feeds directly into one or more of the various tests above.

UK Resident Family

An individual holds a family tie for the Sufficient Ties Test where their spouse, civil partner, or cohabiting partner (excluding separated spouses under a court order or formal deed) is UK resident, or where they have a child under 18 who is UK resident and with whom they spend more than 60 days in the tax year. See the Family Tie section for full detail.

Home and Accommodation

A home under the SRT is a place where you live in a settled and consistent manner. It can be a building, part of a building, a vessel, or any structure used as a home, whether or not you own it, rent it or simply use it for free. A home in the UK is always an Accommodation Tie for the purposes of the Sufficient Ties Test. However, an Accommodation Tie is not necessary a “home” – there is a difference in quality between the two. The term “home” has no precise definition within the SRT, in which case we have to rely on the ordinary meaning of the word (see the Oxford English Dictionary for a possible definition). The law does say that a “home” is not a “holiday home or temporary retreat”, so a property used only occasionally and irregularly is less likely to be a home that one which is used frequently and consistently.

Accommodation (as used in the Accommodation Tie) is broader. It covers any property (owned, rented, a hotel, or accessible at a relative’s home) available for a continuous period of at least 91 days in the tax yea. Gaps of fewer than 16 nights in availability are normally disregarded. The individual must also spend at least one night there during the year.

If you spend at least 16 nights in the home of a single close relative, that will also create an Accommodation Tie for you. It is normal for most British expatriates to have an Accommodation Tie.

Work

Work for SRT purposes covers employment duties, self-employment, directorial activities, travel in connection with work, and training – simply put, anything that your paid or pay yourself to do, regardless of location or length. Voluntary work is generally excluded.

Workday (Day Spent Working in the UK or Overseas)

A workday is any day on which you work for more than three hours in the relevant location. This threshold applies consistently across all work-based tests and the work tie.

Working Sufficient Hours Abroad

This feeds into the third Automatic Overseas Test. It requires an average of 35 or more hours of overseas work per week, calculated over a precisely defined reference period using a detailed five-step method that excludes UK working days and gap days, then divides net overseas working days by the number of weeks. Whilst it is helpful shorthand to say that you must do an average of 35 hours per week or work outside of the UK, the reality is that the precise 5 step process must be followed to be sure whether you qualify. See the Third Automatic Overseas Test section for full detail.

Full-Time Work Abroad (FTWA)

You qualify as being in Full-time Work Abroad if you: (1) do sufficient hours overseas, averaging 35 or more per week; (2) have no significant break from overseas work; and (3) you spend fewer than 91 days in the UK and there are no more than 30 UK working days in the tax year. See the Third Automatic Overseas Test for full conditions.

Working Sufficient Hours in the UK (WSHUK)

Full-time UK work requires: (1) sufficient hours in the UK, averaging 35 or more per week over a 365-day period; (2) no significant break; (3) more than 75% of working days in the UK; and (4) at least one UK working day in the tax year. See the Third Automatic UK Test for full conditions.

Significant Break

A significant break is a period of 31 or more consecutive days on which the individual does not perform work of more than 3 hours in the relevant location if they are self-employed, or are without a contract of employment. Approved leave (holidays and sick leave within an existing employment) is excluded, so these periods do not count toward the 31-day run. An unexplained gap between contracts, or a voluntary absence not covered by approved leave, can constitute a significant break.

Family Tie

An individual holds a family tie where:

- Their spouse, civil partner, or cohabiting partner (excluding separated spouses under a court order or formal deed of separation) is UK resident for the tax year; or

- They have a child under 18 who is lives in the UK and is not in full-time education, and they spend more than 60 days in the tax year with that child, whether in a group or one-to-one; or

- A child under the age of 18 who is in full-time education and that child spends 21 days or more in the UK outside of term time (i.e. during Christmas, Easter and Summer holidays).

Accommodation Tie

An Accommodation Tie exists where:

- UK accommodation is available for a continuous period of at least 91 days in the tax year, whether owned, rented, at a hotel, or through friends and family; and

- The individual spends at least one night there during the year.

Gaps in availability of fewer than 16 nights are disregarded. For accommodation at the home of a close relative (parent, grandparent, sibling, adult child, or adult grandchild), the individual must spend more than 15 nights there (16 or more) for the tie to apply.

Work Tie

A work tie arises where the individual spends 40 or more days working in the UK during the tax year. A UK working day is any day on which more than three hours of work is done in the UK, including days when the individual is not in the UK at midnight.

90-day Tie

The 90-day tie is backward-looking. It arises where the individual spent more than 90 days in the UK in either or both of the two preceding tax years. Exceeding 90 days in just one of those two years is sufficient; it is not a combined total. This tie commonly catches individuals in their first or second year after leaving the UK.

Country Tie

The country tie applies only to Leavers (those who were UK resident in at least one of the preceding three tax years). It arises where the UK is the country in which the individual spends the greatest number of days, or where the UK ties with another country for the highest day count. Where two countries are exactly tied, work days serve as a tiebreaker.

Common Ties for Business Owners and Directors

Business owners and company directors based overseas are disproportionately exposed to accumulating multiple UK ties without realising it:

- A work tie from attending 40 or more days of UK board meetings and business activities.

- A 90-day tie from having spent more than 90 UK days in a prior year, common in the tax year before departing the UK.

- An accommodation tie from a property that remains available throughout the year.

- A family tie if a spouse or partner continues to live in the UK.

A Leaver spending 60 UK days with just three of these four ties is UK resident under the Sufficient Ties Test. This position can often be managed with forward planning, but only if the analysis is done before the year ends, not after.

Arrivers

Arrivers are individuals who were not UK resident in any of the three preceding tax years. Only four ties are relevant under the Sufficient Ties Test; the country tie does not apply. With only four possible ties, the number needed to establish residence is higher relative to UK day count.

Leavers

Leavers are individuals who were UK resident in one or more of the preceding three tax years. All five ties are potentially relevant, including the country tie, which can arise simply from spending more days in the UK than in any other single country. The Arriver/Leaver distinction persists until the individual has been non-resident for three consecutive complete tax years.

Number of UK Ties Needed

The following tables show the minimum number of ties required, for a given UK day count, to be treated as UK resident under the Sufficient Ties Test

UK ties needed if you were UK resident for one or more of the 3 tax years before the tax year under consideration

Days spent in the UK | Ties needed to be UK resident |

Fewer than 16 | Non-resident regardless of ties |

16 to 45 | 4 or more ties |

46 to 90 | 3 or more ties |

91 to 120 | 2 or more ties |

121 to 182 | 1 or more ties |

183 or more | Resident regardless of ties |

UK ties needed if you were UK resident in none of the 3 tax years before the tax year under consideration

Days spent in the UK | Ties needed to be UK resident |

Fewer than 46 | Non-resident regardless of ties |

46 to 90 | All 4 ties |

91 to 120 | 3 or more ties |

121 to 182 | 2 or more ties |

183 or more | Resident regardless of ties |

Reading the tables: a Leaver spending 70 UK days who holds three UK ties is UK resident. The same person with two ties is not.

Split Year Treatment

The default rule under the SRT is that residence status applies for the entire tax year. Split year treatment is the exception: it divides the year into a UK part and an overseas part, with different tax treatment for each. Foreign income and gains arising during the overseas part typically fall outside the UK tax charge.

Split year treatment is available in eight defined cases: three relating to departure (Cases 1 to 3) and five relating to arrival (Cases 4 to 8). It must be claimed on the Self-Assessment return and only applies where you are UK resident for the full tax year under the SRT.

From 6 April 2025, split years count as full UK residence years for the four-year Foreign Income and Gains (FIG) regime and for the long-term residence inheritance tax rules.

Different conditions apply depending on which Split Year Case is relevant. This is complex area and professional advice should be sought. Conditions apply to the Non-Resident part of the tax year as well as to the Resident part, and sometimes also in the prior and following tax years. Real care is needed to ensure that you understand and meet the conditions which are relevant to your case.

How Split Year Treatment Impacts Your Tax Obligations

During the overseas part, you are treated as non-resident: UK-source income remains taxable in the UK. Foreign income and gains arising during the overseas part are generally (but not always) outside the scope of UK tax.

During the UK part, you are fully UK resident: You are taxed on worldwide income and gains in the usual way. However, you may have access to FIG, OWR or Double Tax Treaty relief.

Anti-Avoidance

The SRT includes specific anti-avoidance provisions to prevent individuals from exploiting the structure of the tests. The most significant is the Temporary Non-residence regime.

Temporary Non-Residence and its Tax Implications

Recent Leavers

The temporary non-residence rules apply where:

- The individual was UK resident for at least four of the seven tax years immediately before departure; and

- They return to UK residence within five years of leaving.

Where both conditions are met, certain income and gains arising during the non-resident period are treated as if they arose in the tax year of return, and taxed accordingly.

Temporary Non-Residence Rule

The assets and income caught include:

- Capital gains on assets held before the departure date, realised while non-resident.

- Dividends from close companies where the underlying profits derive from periods of prior UK residence.

- Pension lump sums from Employer Financed Retirement Benefit Schemes (EFRBS).

- Life assurance chargeable event gains arising during the non-resident period.

What is not caught: employment income, regular investment income (bank interest, dividends from listed public companies) that genuinely arose while non-resident, and most day-to-day income.

The rule regularly catches returning expats who assumed that gains realised while non-resident were permanently outside the UK tax net. If you left the UK having been resident for four or more of the previous seven years, realised significant gains abroad, and returned before five complete tax years had elapsed, those gains may be taxable in the year of return. The five-year clock should be confirmed before any return date is fixed. If return within 5 years is unavoidable, the provisions of a Double Tax Treaty could potentially override the Temporary Non-Residence provisions.

Overseas Workday Relief

Overseas Workday Relief (OWR) is available to individuals during their first four tax years of UK resident status where they have previously been non-resident for at least 10 complete and consecutive tax years immediately preceding their relocation to the UK

From April 2025, OWR has been reformed alongside the non-domicile changes. Relief now follows FIG eligibility and is available for the year of arrival in the UK and the following three tax years. The requirement to keep earnings offshore has been removed. Relief is capped at the lower of 30% of employment income or £300,000 per year. Individuals who were previously relying on the remittance basis for OWR should take up-to-date advice to confirm their position under the new rules.

Special Rules for International Transport Workers

International transport workers, including airline crew, seafarers, and long-haul lorry drivers, are subject to modified SRT rules because their working patterns are inherently cross-border. An international transport worker is broadly defined as an individual whose employment requires duties aboard a vehicle, aircraft, or ship in transit, where substantially all journeys cross international boundaries and at least six cross-border trips are made per year.

Two significant modifications apply. First, international transport workers cannot satisfy the full-time overseas work test (AOT 3) or the full-time UK work test (ART 3). Second, for the work tie, any day on which the individual’s journey begins in the UK counts as a UK working day regardless of hours actually worked. Crew based at UK airports will therefore accumulate UK working days quickly, potentially reaching the 40-day threshold for the work tie sooner than the standard rules might suggest.

Crown Servants

Some people are employed by the British Government overseas – diplomatic staff, most commonly. Crown Servants remain taxable in the UK on their employment earnings and they enjoy certain tax privileges. However, it is commonly assumed that foreign posted Crown Servants remain resident in the UK. That is not the case – the SRT applies to Crown Servants in exactly the same way as it does to everyone else, with the tax freedoms that are possible with Non-Resident status in respect of other private incomes and gains.

Transitional Provisions

The SRT took effect on 6 April 2013. For the SRT’s backward-looking tests (prior residency questions in the AOTs, ARTs, and the Arrivers/Leavers distinction), residence in years before 2013/14 is assessed under the rules that applied at the time. These provisions are now largely of historical interest; most individuals subject to the SRT have enough post-2013 tax history for the transitional period to have no bearing on their current position.

Exceptional Circumstances

Up to 60 days per tax year may be disregarded from an individual’s UK day count where those days arise from exceptional circumstances genuinely beyond the individual’s control: a sudden or life-threatening illness, a natural disaster, civil unrest, or other sudden unforeseeable disruption.

What does not qualify:

- An extended stay from a change of plans

- A business reason, however compelling, for staying longer than intended

- Elective medical treatment arranged in advance.

Only days genuinely attributable to the exceptional circumstances can be disregarded. HMRC would expect you to be able to produce contemporaneous evidence if they ask to see it, such as medical records, cancelled flight confirmations, and correspondence documenting why departure was not possible

COVID-19

HMRC confirmed that COVID-19 travel restrictions could qualify as exceptional circumstances. Days when individuals were genuinely unable to leave the UK due to pandemic restrictions could be disregarded from the day count, subject to the 60-day annual cap. Days when the individual chose to remain, rather than being prevented from leaving, did not qualify. Each case required individual assessment; no blanket disregard was available.

The position was assessed separately for 2019/20 and 2020/21. Individuals whose UK presence in either year was swollen by pandemic restrictions, and who did not claim the exceptional circumstances disregard on the relevant Self-Assessment returns, may have returns that can still be amended, depending on whether the amendment window remains open.

How to Prepare for the Statutory Residence Test

The SRT is self-assessed. The individual determines their own status, reports it on the Self-Assessment return, and maintains the evidence to support it if HMRC asks. Preparation is ongoing, not something completed in January when the filing deadline approaches.

Keep Detailed Records

- Travel records: Boarding passes, passport stamps, and itineraries showing UK arrival and departure dates.

- Day count log: A running record of nights in the UK versus overseas, maintained throughout the year. Reconstructing this at year-end is error-prone and harder to defend under enquiry.

- Work records: Timesheets, work diaries, email headers with geographic indicators, and meeting records showing where work was done and for how many hours.

- Accommodation records: Lease agreements, hotel bookings, and utility bills showing when properties were available and occupied.

- Family records: Evidence of the residence status of a spouse or partner, including their employment records and school enrolment documents for children.

Records should be kept for six years.

Review Previous Years

Before working through the SRT tests in any year, confirm: whether you were UK resident in any of the three preceding years (determines which AOT applies and Arriver/Leaver status); how many UK days you spent in each of the two preceding years (determines the 90-day tie); and whether ties held in prior years affect the current year.

Plan Your Travel and Work

- Monitor UK days throughout the year and set personal limits at the key thresholds (16 days, 46 days, 90 days).

- Manage UK working days: keep them below 40 to avoid the work tie. For directors, that means scheduling board attendance carefully and handling as much as possible remotely from overseas.

- Limit accessible UK accommodation: arrangements that fall below 91 continuous days of availability can avoid the accommodation tie altogether.

- Structure travel to avoid overnight stays where the day count is tight: a UK day is counted by presence at midnight, so leaving before midnight can keep a day off the count.

- Consider departure timing in the context of split year cases, as satisfying the conditions from the intended split date requires planning before the tax year begins, not after.

Change of Circumstances

A new role requiring more UK presence, an inherited UK property, a spouse returning ahead of you: each can shift the number of ties held and alter the SRT outcome. Review your SRT position when significant changes occur, not only at return-filing time.

Consult Tax Professionals

For anything other than a straightforward position (multiple homes, international employment, borderline day counts, a year of significant personal change), taking advice before acting is the sensible course. Getting the analysis wrong in a year with borderline counts can produce a tax charge that can substantially outweigh the cost of a proper review.

Statutory Residence Test Penalties and Compliance Risks

If you get your residence status wrong (claiming non-residence when you are in fact resident), HMRC can open an enquiry, assess the unpaid tax, and apply penalties.

- Inaccuracy penalties: These range from 0% (careless error, unprompted disclosure) to 100% of unpaid tax (deliberate error with concealment). For offshore matters, the Failure to Correct regime extended penalties to 200% of unpaid tax in certain circumstances.

- Interest: Runs on unpaid tax from the due date at approximately 7.75% per annum.

- Late filing penalties: Begin at £100, escalate over time, and can include a tax-geared surcharge where significant tax is outstanding.

HMRC’s investigative capabilities are considerable: UK Border Agency records capture entry and exit data; the Common Reporting Standard brings in financial account information from more than 100 jurisdictions; Land Registry confirms property ownership; and Companies House captures directorships. Your claim for Non-Resident status is not automatically referenced through these sources, however, unless HMRC opens an enquiry into your position and makes use of certain investigative powers – which it must disclose to you first.

Your SRT Checklist

Step 1: Determine Your Status

- Establish whether you were UK resident in any of the preceding three tax years (Arriver or Leaver?)

- Count total UK days, including any days caught by the deeming rule

- Identify whether exceptional circumstances days can be disregarded and whether they are documented

- Check whether any Automatic Overseas Test applies

- Check whether any Automatic Residence Test applies

- If neither is conclusive: count UK ties (Family, Accommodation, Work, 90-day, and Country if Leaver) and apply the relevant table

Step 2: Check for Special Rules

- Consider whether split year treatment applies; if so, identify which case and what the split date is

- Review whether the temporary non-residence rules affect any gains or income planned for this year or the year of return

Step 3: Records and Filing

- Ensure records are in order: travel, accommodation, work location, day count log

- File the Self-Assessment return by the deadline, claiming split year treatment if applicable

Why Choose Spice Taxation to Help With the Statutory Residence Test?

- The SRT is at the centre of what we do every day: More than 80% of Spice Taxation’s clients live outside the UK, and the SRT is the first question we work through with almost all of them, whether managing non-residence from their location, planning a return to the UK, or navigating a year where the numbers are uncomfortably close to threshold. It is the foundation of the practice, not an occasional topic. It is the foundation of all tax-efficiency where a person lives abroad.

- Thirty years of residence casework: We have been advising British expats and non-residents since before the SRT existed: through the old common law rules, through the introduction of the test in 2013, and through every legislative change since. That history includes cases that went to dispute and clients whose non-residence positions were reviewed by HMRC and held up under scrutiny. We know where the test produces genuine uncertainty and where the risk of challenge is highest.

- Independent advice, no referral arrangements: We operate without commercial relationships with financial advisers, insurance companies, or property agents. Our advice reflects your position, not a referral arrangement.

FAQs

How do I Prove Non-UK Residency to HMRC?

HMRC does not issue a certificate of non-residence, as the SRT is self-assessed. If your status is ever queried, you will need supporting records to back up your claim: travel documents, a running day count log, work location evidence, and accommodation details. Keep these for at least six years.

I Left the UK Mid-Tax-Year. When Does the Clock Start for My Non-Residence?

Non-residence does not typically begin from the date you leave. Split year treatment changes this: satisfying Case 1 (starting full-time overseas work) or Case 3 (ceasing to have a UK home) splits the year at the departure date. Foreign income and gains after that date fall outside the UK tax charge. Split year treatment must be claimed on the Self-Assessment return.

Do I Need to File a P85 or Self Assessment Return When Leaving the UK?

If you were employed in the UK, filing form P85 when you leave helps close your employment record and may result in a refund of overpaid tax. A Self Assessment return is also required if you have other taxable income, capital gains, or are claiming split year treatment.

Does Renting a Property in the UK Create an Accommodation Tie?

In most cases, yes. An accommodation tie arises where a property is available to you for 91 or more continuous days in the tax year and you spend at least one night there. To avoid it, keep the flat’s availability below 91 continuous days or ensure you spend no nights there during the year.

Can I Remain a UK Company Director While Non-Resident?

Yes, holding a UK directorship does not affect your residence status per se. That said, attending UK board meetings in person counts as UK working days, and exceeding 40 of those in a tax year creates a work tie. Where possible, handling board matters remotely avoids this.

Does Spending Time in the UK for Medical Treatment Count Toward My Day Count Under the SRT?

Unforeseen daysays spent in the UK due to a sudden or life-threatening illness can be excluded from your UK day count, up to the 60-day annual cap. Pre-planned or elective treatment does not. HMRC expects supporting evidence: medical records, clinical correspondence, and travel records confirming departure was not clinically safe.

How Does SRT Apply to Deceased Persons?

Modified rules apply in the year of death. AOT 1 does not apply; AOT 4 and AOT 5 apply instead, based on prior non-residency and overseas work at the time of death. The Fourth Automatic UK Test treats the individual as UK resident where they were automatically resident in each of the three previous years and held a UK home at death. Where the Sufficient Ties Test applies, day-count thresholds are reduced proportionally.

Does a Double Tax Treaty Override the SRT?

Yes and No. The SRT determines your UK tax residence under domestic law and a treaty does not change that. However, where you are also treated as resident in another country, a tie-breaker clause in the relevant treaty may limit HMRC’s ability to tax certain income and gains. Treaty protection must be actively claimed and is fact-specific.

References

HM Revenue & Customs. (2013). RDR3: Statutory Residence Test (SRT): Guidance Note. GOV.UK. https://www.gov.uk/government/publications/rdr3-statutory-residence-test-srt/guidance-note-for-statutory-residence-test-srt-rdr3

UK Parliament. (2013). Finance Act 2013, Schedule 45. legislation.gov.uk. https://www.legislation.gov.uk/ukpga/2013/29/schedule/45